How to Build a 6-Month Emergency Fund

How to Build a 6-Month Emergency Fund

As we navigate our 40s and 50s, financial security becomes increasingly important. One of the most crucial elements of financial stability is having a well-funded emergency savings account. According to Bankrate’s 2025 Annual Emergency Savings Report, around 3 out of 10 Gen Xers (ages 44-59) have no emergency savings at all, while 27% of Americans wouldn’t be able to cover a month’s worth of expenses if they lost their job tomorrow .3 .1.

Building a six-month emergency fund might seem daunting, but it’s an achievable goal with the right strategy and mindset. This comprehensive guide will walk you through practical steps to establish this essential financial safety net.

Why a Six-Month Emergency Fund Matters at Midlife

In our 40s and 50s, emergency funds become even more crucial. At this stage of life, we often have more financial responsibilities and potentially less time to recover from financial setbacks before retirement.

The Stakes Are Higher Now

Emergency funds are arguably even more important as we approach retirement age, as job loss could mean longer periods of unemployment or having to accept lower-paying positions .1. Additionally, unexpected healthcare costs tend to increase as we age, making financial preparedness essential.

Real Protection Against Life’s Uncertainties

From a broken refrigerator to emergency dental work, unexpected expenses can arise at any time. In fact, more than 1 in 3 U.S. adults (37%) used their emergency savings in the past 12 months, with millennials and Gen Xers being the most likely to tap into these funds .6. Having six months of expenses saved provides a substantial buffer against these financial shocks.

Determining Your Emergency Fund Goal

Calculate Your Essential Monthly Expenses

Start by calculating your essential monthly expenses. This includes:

-

Housing (mortgage or rent)

-

Utilities

-

Food

-

Transportation

-

Insurance premiums

-

Minimum debt payments

-

Essential healthcare costs

Multiply this figure by six to determine your target emergency fund amount. For example, if your monthly expenses total $2,500, your six-month emergency fund goal would be $15,000 .4.

Adjusting Your Goal Based on Personal Circumstances

While six months is a standard recommendation, your specific situation might call for adjustments:

Consider increasing your goal if you:

-

Are self-employed or have variable income

-

Work in a specialized field with limited job opportunities

-

Have health conditions that might require costly care

You might aim for a smaller fund if you:

-

Have minimal monthly expenses

-

Have no dependents

-

Are in a dual-income household

-

Work in a high-demand field with abundant job opportunities .3

Creating a Strategic Savings Plan

Start Small, Think Big

If saving six months of expenses feels overwhelming, begin with a more manageable goal. Set an initial target of $500 or $1,000, which can cover many common emergencies like car repairs or minor medical expenses .2. Once you reach this milestone, you’ll gain momentum and confidence to continue building toward your larger goal.

Establish a Dedicated Account

Your emergency fund should be kept separate from your regular checking account to reduce the temptation to spend it. Consider these options:

-

High-yield savings account: Provides liquidity and earns interest

-

Money market account: Often offers higher interest rates while maintaining accessibility

-

Short-term certificates of deposit (CDs): For portions of your emergency fund that you’re less likely to need immediately .4 .6

Automate Your Savings

Set up automatic transfers from your checking account to your emergency fund. This “pay yourself first” approach ensures consistent progress toward your goal without requiring constant decision-making .4. Even small regular contributions add up significantly over time.

Accelerating Your Emergency Fund Growth

Find Extra Money in Your Current Budget

Examine your spending habits to identify potential savings:

-

Review and cancel unused subscriptions

-

Reduce dining out frequency

-

Postpone non-essential purchases

-

Comparison shop for insurance and other services

-

Refinance high-interest debt .5

Leverage Windfalls and Extra Income

Commit to saving a significant portion of any unexpected money:

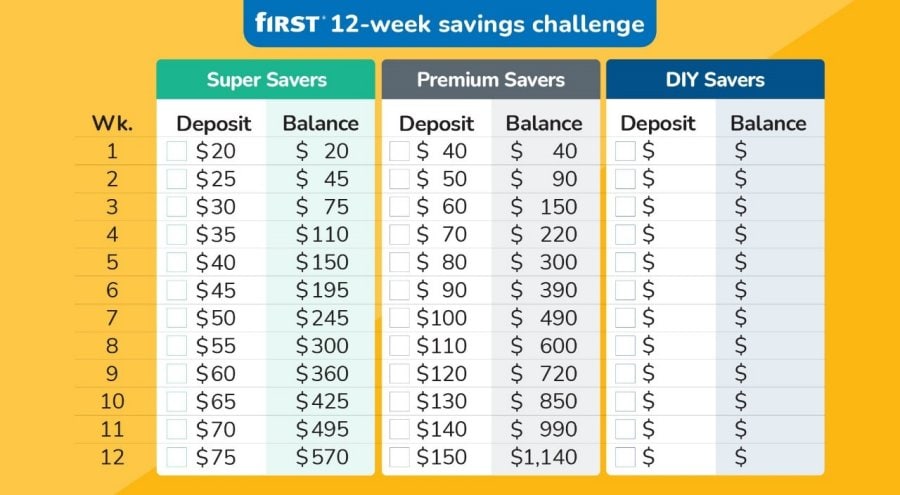

Implement Savings Challenges

Make saving more engaging by turning it into a challenge:

-

No-spend days (designate one day weekly when you don’t spend money)

-

The 52-week savings challenge (save $1 in week one, $2 in week two, etc., resulting in $1,378 saved by year-end) .10

Protecting and Optimizing Your Emergency Fund

Balance Accessibility with Growth

Your emergency fund needs to be readily available when needed, but that doesn’t mean it can’t work for you:

-

Shop for competitive interest rates: Compare high-yield savings accounts from different financial institutions

-

Consider bank accounts with bonus tiers: Some banks offer increased interest rates when you meet certain criteria, such as direct deposit of your paycheck or maintaining minimum balances .10

-

Guard against inflation: While keeping most of your emergency fund liquid, consider investing a portion in assets that might better keep pace with inflation, such as Treasury Inflation-Protected Securities (TIPS) .5

Establish Clear Usage Guidelines

Define what constitutes a true emergency to avoid dipping into your fund for non-essential expenses. According to Bankrate’s survey, the majority (80%) of people who used their emergency savings in the past year did so for essentials like unplanned emergency expenses (51%), monthly bills (38%), or day-to-day expenses (32%) .6.

Replenish Promptly After Use

If you need to use your emergency fund, make replenishing it a top priority. Create a plan to rebuild your savings as quickly as possible to ensure you remain protected against future emergencies .5.

Overcoming Common Obstacles

Dealing with Competing Financial Priorities

Many people in their 40s and 50s face multiple financial demands, including:

-

Saving for retirement

-

Paying for children’s education

-

Supporting aging parents

-

Paying down debt

While these are all important, having an emergency fund is fundamental t