Savings Strategies 50-30-20 for Middle-aged Adults

Savings Strategies 50-30-20 for Middle-aged Adults

Middle age brings unique financial challenges and opportunities. As you navigate your 40s and 50s, you’re likely juggling multiple financial responsibilities while trying to prepare for retirement. The 50-30-20 budgeting rule offers a straightforward framework that can help you manage your finances effectively during this crucial period of your life.

Understanding the 50-30-20 Rule

The 50-30-20 rule is a simple yet powerful budgeting strategy popularized by U.S. Senator Elizabeth Warren in her book, “All Your Worth: The Ultimate Lifetime Money Plan.” .1 This intuitive approach divides your after-tax income into three key categories:

-

50% for Needs: Essential expenses you must pay for survival and basic living

-

30% for Wants: Non-essential items that enhance your quality of life

-

20% for Savings: Money set aside for future financial goals and security

This balanced approach ensures you’re covering necessities while still enjoying life and building for the future—a particularly important balance to strike during middle age.

Why the 50-30-20 Rule Works for Middle-aged Adults

For adults in their 40s and 50s, this budgeting method offers several advantages:

-

Simplicity: The straightforward framework makes it easy to implement without complex calculations or tracking systems .1

-

Balance: It acknowledges the need for both present enjoyment and future planning—crucial during middle age when both immediate responsibilities and retirement planning are priorities

-

Flexibility: The percentages serve as guidelines that can be adjusted based on your specific circumstances and financial goals

-

Financial awareness: Following this rule helps you become more conscious of your spending habits and financial priorities .3

Breaking Down the 50-30-20 Rule for Middle Age

The 50%: Managing Essential Needs

Half of your after-tax income should cover your necessities—the bills you absolutely must pay. For middle-aged adults, these typically include:

-

Mortgage or rent payments

-

Car payments and transportation costs

-

Groceries

-

Insurance (health, auto, home)

-

Utilities

-

Minimum debt payments .1

Middle Age Consideration: At this stage of life, you may be facing higher essential expenses than younger adults. Many in their 40s and 50s are still paying mortgages, potentially helping with college expenses for children, and possibly beginning to face increased healthcare costs. Carefully evaluate what truly constitutes a “need” versus a “want” in your budget.

If your needs exceed 50% of your income, consider whether some expenses can be reduced or if certain “needs” might actually be “wants” in disguise. For example, while a car is often necessary, a luxury vehicle with high payments might fall more into the “wants” category.

The 30%: Balancing Wants

This category covers non-essential expenses that make life more enjoyable but aren’t absolutely necessary for survival. For middle-aged adults, these might include:

-

Dining out and entertainment

-

Streaming services and cable TV

-

Shopping for non-essential items

-

Hobbies and recreational activities

Middle Age Consideration: As your income potentially peaks during these years, the temptation to increase lifestyle spending can be strong. However, middle age is also when retirement planning becomes more urgent. Be mindful of lifestyle inflation and consider whether some “wants” spending might better serve you in the “savings” category.

:max_bytes(150000):strip_icc()/FinanceYourFuture-LifestyleInflation-v12-b99d165f4b1f4f4eb4b861acccbc13e3.png)

The 20%: Prioritizing Savings and Financial Goals

This crucial category focuses on building financial security and preparing for the future. For middle-aged adults, this typically includes:

-

Retirement contributions (401(k), IRAs)

-

Emergency fund maintenance

-

Debt reduction beyond minimum payments

-

Investment accounts

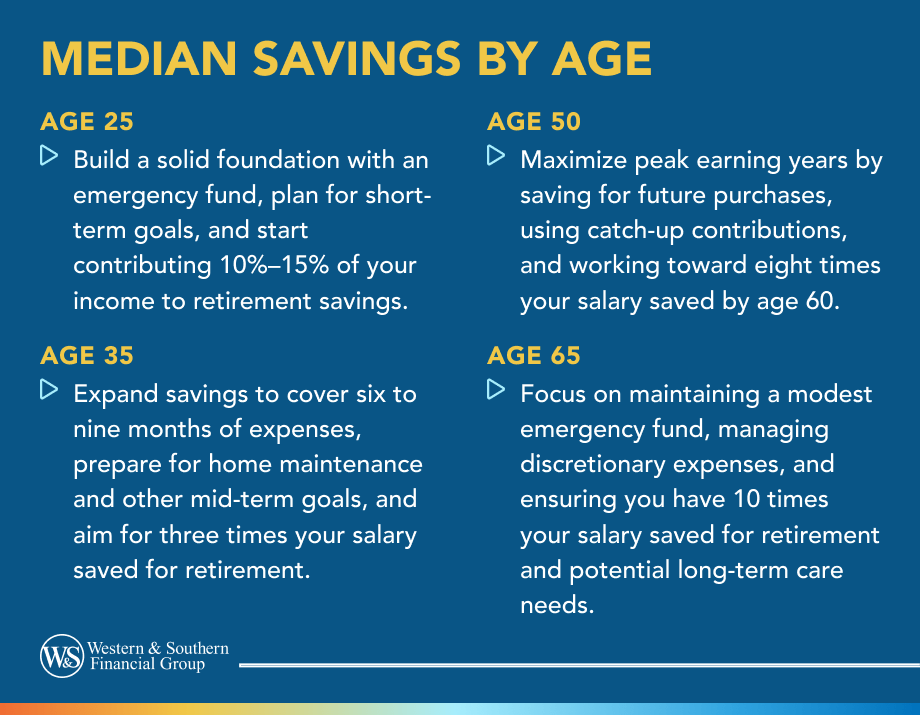

Middle Age Consideration: Financial experts often suggest that by your 40s, you should have approximately three times your annual salary saved for retirement. .6 If you’re behind on retirement savings, you might need to allocate more than 20% to this category. This is particularly important as you enter your peak earning years, which present a valuable opportunity to catch up on savings.

Practical Implementation for Middle-aged Adults

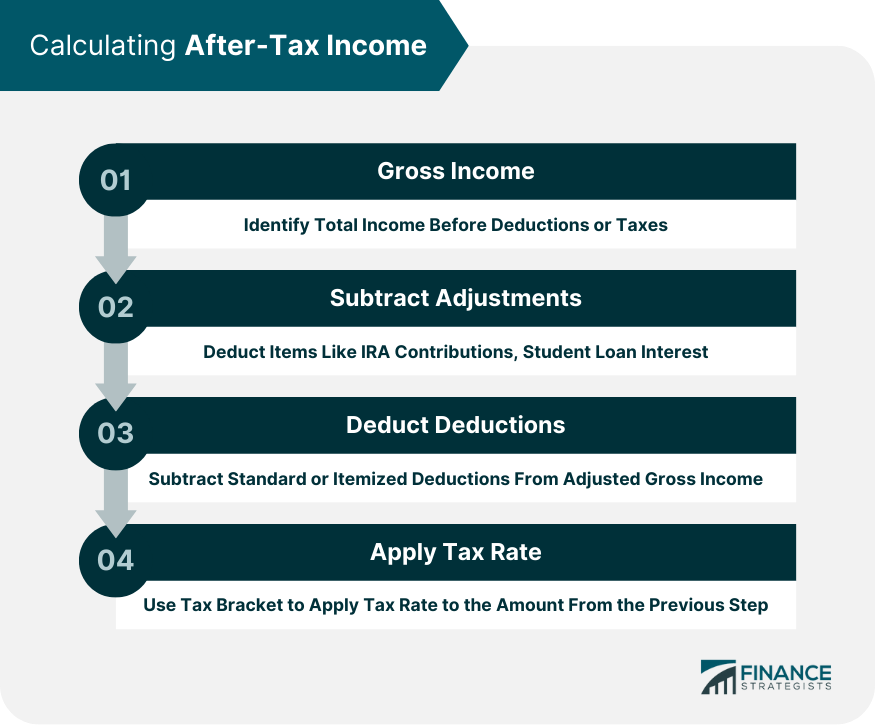

Step 1: Calculate Your After-Tax Income

Start by determining your actual take-home pay after taxes and other deductions. For many middle-aged adults with multiple income sources, this might include:

-

Salary or wages

-

Side business income

-

Investment income

-

Rental property income

-

Any other regular income sources

Step 2: Track Your Current Spending

Before implementing the 50-30-20 rule, understand where your money is currently going. For at least one month, track all expenses to get a clear picture of your spending habits. .14 This can be eye-opening and help identify areas where adjustments are needed.

Step 3: Categorize and Adjust Your Spending

Once you know your current spending patterns, categorize each expense as a need, want, or savings contribution. Then adjust as necessary to align with the 50-30-20 framework.

Example for a $6,000 Monthly After-Tax Income:

-

Needs (50%): $3,000

-

Wants (30%): $1,800

-

Savings (20%): $1,200

Step 4: Set Up Systems for Success

Make your budget work automatically by:

-

Setting up automatic transfers to savings accounts

-

Using separate accounts for different spending categories

-

Utilizing budgeting apps that can categorize expenses

-

Reviewing your budget regularly and making adjustments as needed

Special Considerations for Middle-aged Adults

Sandwich Generation Pressures

Many middle-aged adults find themselves in the “sandwich generation,” simultaneously supporting aging parents and adult children. According to an AARP survey, 32% of adults aged 40-64 provided regular financial support to their parents in the past year, while 51% were still providing money to adult children aged 25 or older. .11

This reality creates additional financial strain during a crucial wealth-building period. If you’re facing these pressures, consider:

-

Having open conversations with family members about financial boundaries

-

Exploring community resources and government programs that might provide assistance

-

Potentially adjusting your 50-30-20 percentages temporarily while maintaining some commitment to savings

Retirement Catch-Up Strategies

If you’re behind on retirement savings, middle age offers important catch-up opportunities:

-

Take advantage of catch-up contributions allowed for those over 50

-

Consider whether you might need to allocate more than 20% to savings

-

Explore whether delaying retirement by a few years might be beneficial

-

Evaluate whether downsizing housing or other major expenses could free up more savings capacity

Healthcare Planning

As healthcare costs tend to increase with age, middle-aged adults should pay special attention to this aspect of financial planning:

-

Maximize contributions to Health Savings Accounts (HSAs) if eligible

-

Ensure adequate health insurance coverage

-

Begin researching long-term care insurance options

-

Include potential healthcare costs in retirement planning calculations .6

Making the 50-30-20 Rule Work for You

Adapting the Percentages

While 50-30-20 provides an excellent framework, your personal situation might require adjustments. Some middle-aged adults might benefit from a 60-20-20 or 40-30-30 split, depending on their specific circumstances and goals. .13 The key is maintaining the discipline of intentional allocation rather than adhering rigidly to specific percentages.

Gamifying Your Savings

Make saving more engaging by turning it into a challenge:

-

Try a “no-spend day” once a week and transfer the savings to your accounts

-

Challenge yourself to a “keep the change” system where you round up purchases and save the difference

-

Use the 24-hour rule for non-essential purchases to reduce impulse buying .10 .12

Leveraging Technology

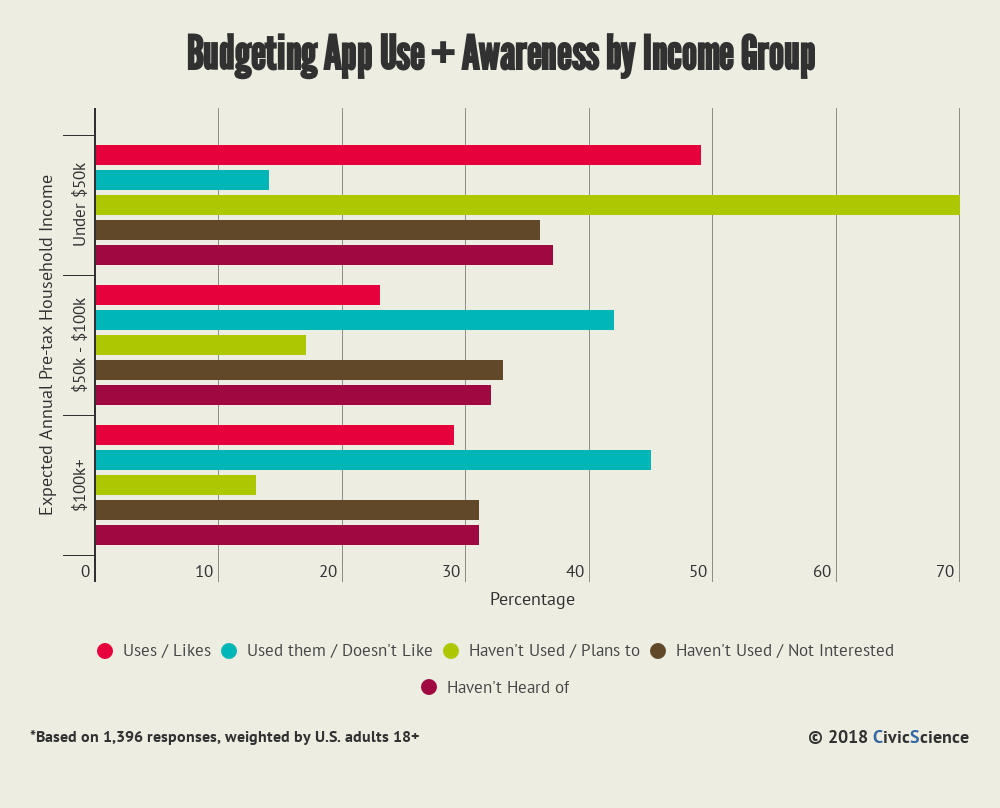

Numerous apps and online tools can help middle-aged adults implement the 50-30-20 rule effectively:

-

Budgeting apps that automatically categorize expenses

-

Round-up savings apps that make saving automatic and painless

-

Investment platforms that simplify retirement planning

-

Spending trackers that provide insights into your habits

The Long-term Impact

Implementing the 50-30-20 rule during middle age can have profound effects on your financial future. By consistently allocating 20% (or more) to savings and debt reduction, you’re building a foundation for:

-

A more comfortable retirement

-

Reduced financial stress

-

Greater ability to handle unexpected expenses

-

Potential financial independence at an earlier age

-

More options regarding work and lifestyle as you approach traditional retirement age

Conclusion

The 50-30-20 rule offers middle-aged adults a balanced approach to managing finances during a critical life stage. By allocating 50% to needs, 30% to wants, and 20% to savings, you create a framework that acknowledges current responsibilities while preparing for the future.

As you implement this strategy, remember that the rule is meant to serve as a guideline rather than a rigid formula. Adapt it to your unique circumstances, regularly review your progress, and make adjustments as your financial situation evolves. With consistent application, this simple budgeting approach can help you navigate the complex financial landscape of middle age while building toward a secure and comfortable future.

The most important step is to begin. Start today by tracking your spending, categorizing your expenses, and making a plan to align your financial habits with your long-term goals. Your future self will thank you for the financial discipline you practice today.